If there is one finance term that sounds simple but quietly controls the day to day survival of a business, it is working capital. People hear it in board meetings, banker calls, or late night accounting chats, but very few slow down to really unpack it. The working capital formula is not just a textbook idea. It shows whether a company can breathe tomorrow morning or struggle to pay bills by Friday. This guide walks through the working capital formula in a relaxed, real world way, without making it feel like a finance exam.

What Is Working Capital?

At its core, working capital is the money a business uses to handle everyday work, not for big long term dreams or five year expansion plans, but for simple things like paying salaries, restocking shelves, clearing utility bills, and managing short term financial obligations without that feeling of panic creeping in, accrued expenses.

The working capital formula sits at the center of this idea, accrued expenses. The working capitals simply compares what a business owns in the short term versus what it owes soon, accrued expenses. When people talk about working capitals in casual business conversations, they usually mean this buffer that keeps operations smooth, accrued expenses.

Working capitals comes from financial assests that are expected to turn into cash within a year. These include cash itself, accounts receivable, and inventory waiting to be sold. On the other side sit current liabilities like supplier dues, short term loans, and accrued expenses. The working capital connects these pieces into one number that tells a story.

Working Capital Explained

The working capitals is straightforward, almost suspiciously simple, financial assests. Working capital equals current assets minus current liabilities, financial assests. That single line explains why businesses obsess over their company balance sheet every month, financial assests.

When current assets are higher, the working capital formula shows a positive figure which usually means the business can manage surprises, delayed payments, or seasonal dips, financial assests. When current liabilities grow faster, the working capital formula turns negative, and stress begins to show up in meetings, financial assests.

People sometimes misunderstand working capital and confuse it with profit. They are different things. A company can be profitable on paper and still struggle with working capitals because cash is locked in inventory or accounts receivable. This is why working capitals become a daily habit, not a once a year review.

Why Is Working Capital Important?

Working capitals matter because bills do not wait. Vendors expect payments, employees expect salaries, and banks expect interest on time. The working capital formula shows whether a business can meet these financial obligations without borrowing again.

Strong working capitals support smoother cash flow forecasting. When leaders know how much buffer exists, decisions feel calmer and less reactive. Weak working capital forces rushed loans, delayed supplier payments, or tough negotiations.

The working capital formula also matters to outsiders. Banks, investors, and even suppliers glance at it before trusting a company. A healthy working capital formula builds confidence that the business can stand on its own feet.

Advantages of Working Capital

Healthy working capitals give businesses flexibility, financial obligations. They allow faster responses to sudden opportunities or emergencies, financial obligations. If a supplier offers a discount for early payment, strong working capital management makes it possible, financial obligations.

Another advantage is credibility. Companies with stable working capitals are seen as reliable partners. Their company balance sheet does not raise red flags. The working capital formula quietly supports long term relationships.

Finally, working capitals help reduce financial anxiety and cash flow forecasting aligns with reality, leaders can focus on growth instead of survival, financial obligations.

Working Capital and the Balance Sheet

The company balance sheet is where the working capital formula lives. Everything needed for the working capital formula is already there. Current assets sit at the top, followed by current liabilities just below.

Financial assests like cash, inventory, and accounts receivable shape the positive side of the working capital. Short term debts, accrued expenses, and payables shape the negative side. Together, they reveal how balanced or strained the business truly is.

Looking at the company balance sheet regularly helps prevent surprises. Working capitals is not about guessing. It is about reading what the numbers quietly say.

How to Calculate Working Capitals

To calculate working capitals, one uses the working capital formula directly from the balance sheet, company balance sheet. The working capital equals current assets minus current liabilities, company’s balance sheet. That is it, no tricks, company balance sheet.

Suppose current assets total one hundred thousand and current liabilities total forty thousand. The working capital formula shows sixty thousand in working capitals. That difference supports daily operations.

The working capitals can be used monthly, quarterly, or even weekly for tight cash environments, company balance sheet. Repeating the working capital formula often keeps small problems from becoming large ones, company balance sheet.

Elements Included in Working Capitals

Understanding the working capital formula requires knowing what goes into it. Not everything on the balance sheet qualifies.

Current Assets

Current assets are financial assests expected to convert into cash within one year. Cash itself is obvious. Accounts receivable matter because unpaid invoices still count as expected cash. Inventory also belongs here, even if it moves slowly sometimes.

These current assets shape the positive side of the working capital formula. If accounts receivable grow too large, the working capital may look fine while actual cash feels tight.

Current Liabilities

Current liabilities include obligations due within a year. These include supplier payables, short term loans, and accrued expenses. Accrued expenses often sneak up on businesses because they feel invisible until payment day arrives.

These current liabilities reduce working capitals directly. When current liabilities rise faster than assets, the working capital formula weakens.

Working Capitals Challenges

Even well run companies struggle with working capital management at times. The working capital formula reflects these struggles clearly.

External Disruptions

Supply chain delays, market slowdowns, or policy changes can hurt working capitals. The working capital formula reacts quickly to such shocks, sometimes before leaders emotionally accept the change.

Poor Cash Flow Management

Weak cash flow forecasting often leads to surprises. Businesses may show positive working capitals on paper while running out of cash. The working capital formula alone cannot fix discipline issues.

Substandard Lending Practices

Relying too heavily on short term debt increases current liabilities. This weakens the working capital formula and increases risk. Sustainable working capital management avoids constant borrowing.

Inaccurate Forecasting

Overestimating sales inflates accounts receivable projections. The working capital formula then looks healthier than reality. When payments delay, stress follows.

Ineffective Inventory Management

The working capital formula includes inventory, but cash feels missing. This is a common trap in retail and manufacturing.

Working Capitals Example

Imagine a company with cash of twenty thousand, accounts receivable of thirty thousand, and inventory of fifty thousand, cash flow forecasting. Total current assets equal one hundred thousand, cash flow forecasting. Current liabilities include payables of thirty thousand and short term debt of ten thousand, cash flow forecasting.

Using the working capital formula, one hundred thousand minus forty thousand equals sixty thousand, cash flow forecasting. This working capital formula result suggests healthy working capitals, assuming inventory moves and receivables collect on time, cash flow forecasting.

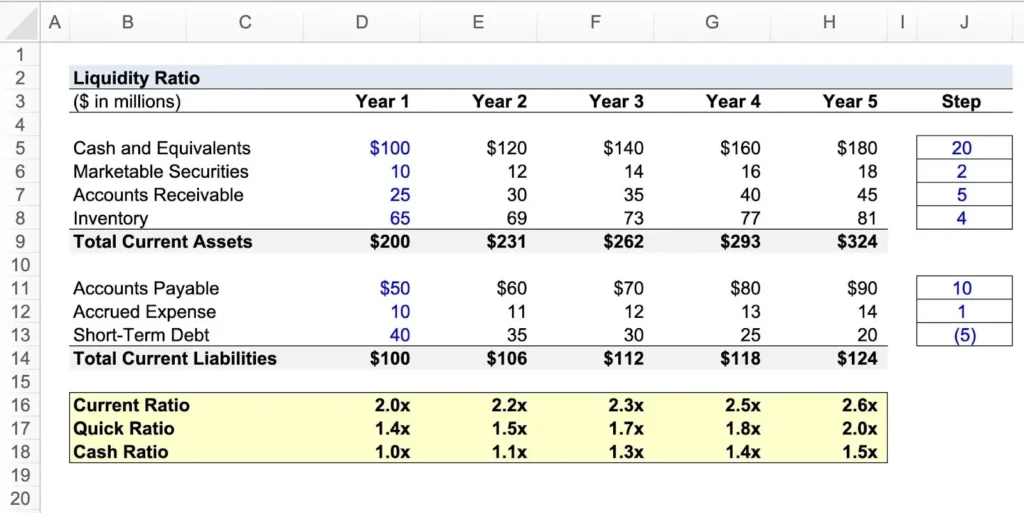

Working Capitals: The Quick Ratio and Current Ratio

Ratios support the working capital formula by adding context.

Quick Ratio

The quick ratio removes inventory from current assets. It tests whether immediate financial assests can cover current liabilities. It is stricter than the working capital formula and useful in cash sensitive industries.

Current Ratio

The current ratio compares current assets to current liabilities directly. While the working capital formula shows a number, this ratio shows proportion. Both matter in working capital management.

Working Capitals vs. Net Working Capital (NWC): What is the Difference?

Net working capital and working capitals often mean the same thing in practice. Net working capital usually refers to the same working capital formula of current assets minus current liabilities.

Some professionals prefer the term net working capital to emphasize clarity. Either way, the working capital formula remains unchanged and central.

Conclusion

Working capital is not something flashy or exciting, but it quietly decides if a business feels steady or constantly stressed out. The working capital formula helps turn everyday money movements into something you can actually see and understand, and by knowing how current assets and current liabilities work together, businesses get better control over their short term future. Good working capital management, along with clear cash flow forecasting and simple balance sheet awareness, helps companies stay grounded, and in the end the working capital formula is less about tricky math and more about peace of mind.

FAQ

How to calculate working capitals?

Working capital is calculated using the working capital formula, which subtracts current liabilities from current assets listed on the company balance sheet.

What is the working capital ratio?

The working capital ratio compares current assets to current liabilities which supports the working capital formula by showing balance rather than absolute value.

What do you mean by working capitals?

Working capital refers to funds available for daily operations after covering short term financial obligations.

What are the four main components of working capitals?

Cash, accounts receivable, inventory, and current liabilities including accrued expenses shape working capitals.

What is the working capitals formula with example?

The working capital formula equals current assets minus current liabilities For example, one hundred thousand minus forty thousand equals sixty thousand.

Is negative working capitals always bad?

Not always. Some fast moving businesses operate with negative working capitals by collecting cash before paying suppliers.